6月19日

3pm - 4pm

研討會, 演講, 講座

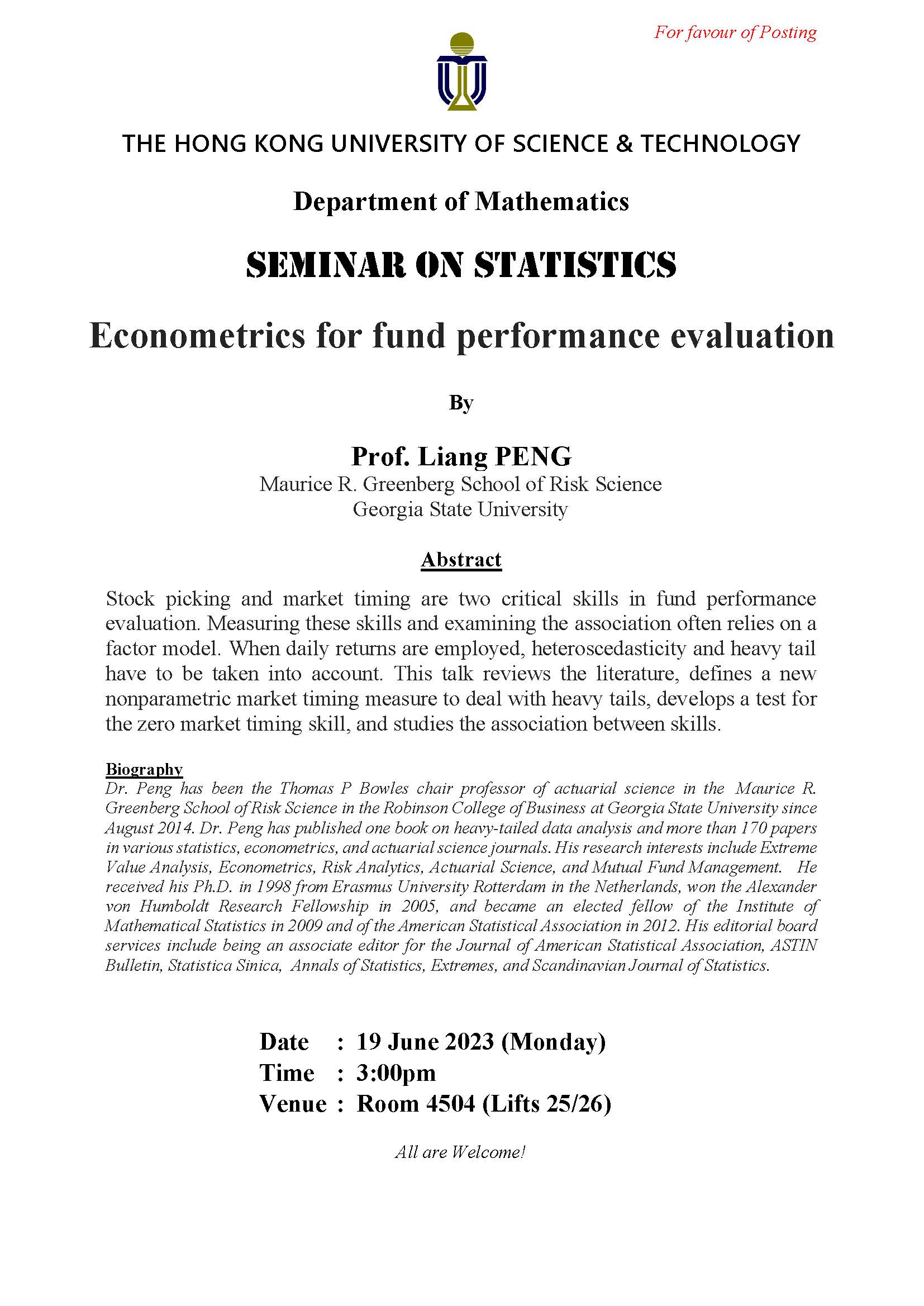

Stock picking and market timing are two critical skills in fund performance evaluation. Measuring these skills and examining the association often relies on a factor model. When daily returns are employed, heteroscedasticity and heavy tail have to be taken into account. This talk reviews the literature, defines a new nonparametric market timing measure to deal with heavy tails, develops a test for the zero market timing skill, and studies the association between skills.

6月19日

3pm - 4pm

地點

Room 4504 (Lifts 25/26)

講者/表演者

Prof. Liang PENG

Maurice R. Greenberg School of Risk Science, Georgia State University

Maurice R. Greenberg School of Risk Science, Georgia State University

主辦單位

Department of Mathematics

聯絡方法

付款詳情

對象

Alumni, Faculty and staff, PG students, UG students

語言

英語

其他活動

6月21日

研討會, 演講, 講座

IAS / School of Science Joint Lecture - Alzheimer’s Disease is Likely a Lipid-disorder Complication: an Example of Functional Lipidomics for Biomedical and Biological Research

Abstract

Functional lipidomics is a frontier in lipidomics research, which identifies changes of cellular lipidomes in disease by lipidomics, uncovers the molecular mechanism(s) leading to the chan...

5月24日

研討會, 演講, 講座

IAS / School of Science Joint Lecture - Confinement Controlled Electrochemistry: Nanopore beyond Sequencing

Abstract

Nanopore electrochemistry refers to the promising measurement science based on elaborate pore structures, which offers a well-defined geometric confined space to adopt and characterize sin...